Blockchain technology often resembles cryptocurrency, its important impact on our fragile environment through mining and misuse in somehow non-legitimate activities.

It’s not often that blockchain technology is related to business and enterprises. But through dedicated blockchain enterprise platforms that can overcome all the pitfalls above, it has the potential to change forever the way we operate business globally (as well as B2B) as much as the internet, cloud or artificial intelligence have all been doing across industries.

This article aims to share how Ericsson has been using state of art of enterprise blockchain technology and its yet not fully developed abilities to change our business interactions with our partners, clients, and suppliers with unparalleled benefits for all parties involved.

In this article, we’ll explore:

1. Business processes and current flaws

2. Main capabilities of blockchain technology: the triad.

3. How Ericsson has been adopting blockchain technology

Business processes and current flaws

Business processes are the beating hearts of any company and are essential to the success of any business execution. They represent the backbone and pillars on which true business efficiency is carried. Let’s deconstruct business processes in building blocks and pinpoint the current weakness.

We’ll start with a simple definition of business process and its founding elements:

Definition:

A business process is a series of interlinked steps which are assigned to every stakeholder for specific work to deliver a product or service to a third party (for example, a business partner, client, or supplier).

For each stakeholder or group of contributors, it’s expected to perform specific task(s) to achieve a concrete goal. See Figure 1 below.

These steps are often repeated many times by multiple users in a standardized and optimized way, following the policy (a set of pre-defined rules) of the business process.

Figure 1: Each stakeholder or group of contributors is expected to perform specific task(s) to achieve a concrete goal.

Examples here include Ericsson’s hiring processes, its supply chains, product development, and product/service delivery.

Most of the time, business processes today run in silos from one step to the next, from one organization to the next, from a company to its partner and client. This can cause faulty or inconsistent outcomes and consequently the need to rework, fault-detect and correct these outcomes. This results in high inefficiency in terms of cost, the time it takes to validate the rules of the underlying process and the consistency of the end-to-end flows.

This is even more evident for processes running across companies, where the lack of trust between the parties prevents true and transparent integration in all steps of the process. This also includes organizations within the same company, where more often than not, they pursue different objectives and goals. For the big corporates, they can even have different or separate legal entities.

The following flaws in a business process can often be recognized:

- Lack of data integration and data integrity

Underlying data layer supporting processes are often ‘broken’ due to lack of integration between the parties. Integrating a data layer in a process is often not only a technical challenge and cost, but a very hard task to enforce organizations with different objectives and interests to share their data (full transparency, not necessarily within a company, is a good thing due to the sensitivity of some data, for instance. Corporates as well as organizations within a company, might need privacy, ensuring appropriate visibility of the underlying data layer).

The lack of data layer integration prevents data consistency across the process, which can cause inconsistency, inefficient and ineffective replication of data when available, as well as potential flaws.

- Poor standardization and compliance

Local regulations, country laws, or cultural attitudes prevent a standardized way of working between the parties running the process. Turning to a local adaptation on the execution of a process can deviate from a common governance and a straight path to reach a common goal. Moreover, in such recurrent scenarios, compliance is often highly affected, heading to costly fines during audits.

- No step-by-step rule validation

A simple fault of a task occurring in a single step of the process without preventative controls may have devasting chain reaction effects on the result of the whole process execution.

No matter how detailed the instructions of the steps in the process procedure are, a sneaky error may have drastic and dramatic consequences in a process execution, and would require rework to find the errors, correct them, and execute it again.

Main capabilities of blockchain technology: the triad

In this section, we’ll focus on the main three enterprise blockchain capabilities, marking blockchain technology as a unique asset in the enterprise architecture landscape.

The Ledger

In essence, blockchain technology is a transaction record mechanism.

As a very first approximation, the ledger is the ‘database’ of blockchain architecture – its repository of the records.

Unique characteristics of the ledger:

- Immutability. Every record of the ledger cannot be changed or deleted. Database CRUD (Create, Read, Update and Delete) is not fully supported; blockchain supports ‘read’ and ‘write’ operations with no ‘update’ or ‘delete’ atomic operations like in ordinary database.

- Distributed. Every member (or organization, in case of enterprise blockchain) owns its copy of the ledger versus the classic client-server database architecture. Ledger distribution prevents central authorities (for example, DBA – Database Administrator) to affect – maliciously or benevolently – the whole data. If an inconsistency happens, blockchain technology will identify and correct the unreliable records (technically this is achieved through ‘consensus mechanisms’ embedded into the distributed architecture). This characteristic fosters the disintermediation between the members of the blockchain network.

Security

- Every record in the ledger is authenticated, verifiable and hashed. Authentication, Authorization and Audit, as well as Non-Repudiation (providing proof of the origin and integrity of the data) are fundamental assets of blockchain technology.

- Cryptography makes the verification and integrity of data, practically impossible to tamper with.

- Transactions are secured through digital signatures assigned to any member of the network, preventing records that can be altered.

Smart Contract

This term, coined in the 1990s by the cryptographer Nick Szabo, refers to “a set of promises, specified in digital form, including protocols within which the parties perform on these promises” [Ref. 1, 2].

In simpler terms, Smart Contract is a computer program stored on a blockchain, automatically executing, validating and taking actions according to agreements between members belonging to the blockchain network.

Smart contracts can interact with external sources to validate rules coded in smart contracts.

All the characteristics above: ledger, security and Smart Contract, bring trust between the parties. This trust is not related to any so-called “man-in-the-middle” or central authority and governance, but rather delegated to the underlying technology and code execution.

How Ericsson has been adopting blockchain technology

It’s time to bring business processes and blockchain technology together, and reveal how Ericsson started using blockchain technology.

Most of the flaws we’ve identified in ordinary business processes can be addressed through blockchain technology.

The siloed approach of many current business processes can be broken through a ‘common source of truth’ – namely the ledger. Despite being physically distributed, the ledger is logically centralized (i.e. ‘the common source of truth’), securing integrity of the underlying data, integration, confidentiality (also known as ‘transparency on a need to know basis’), between the parties involved in the process.

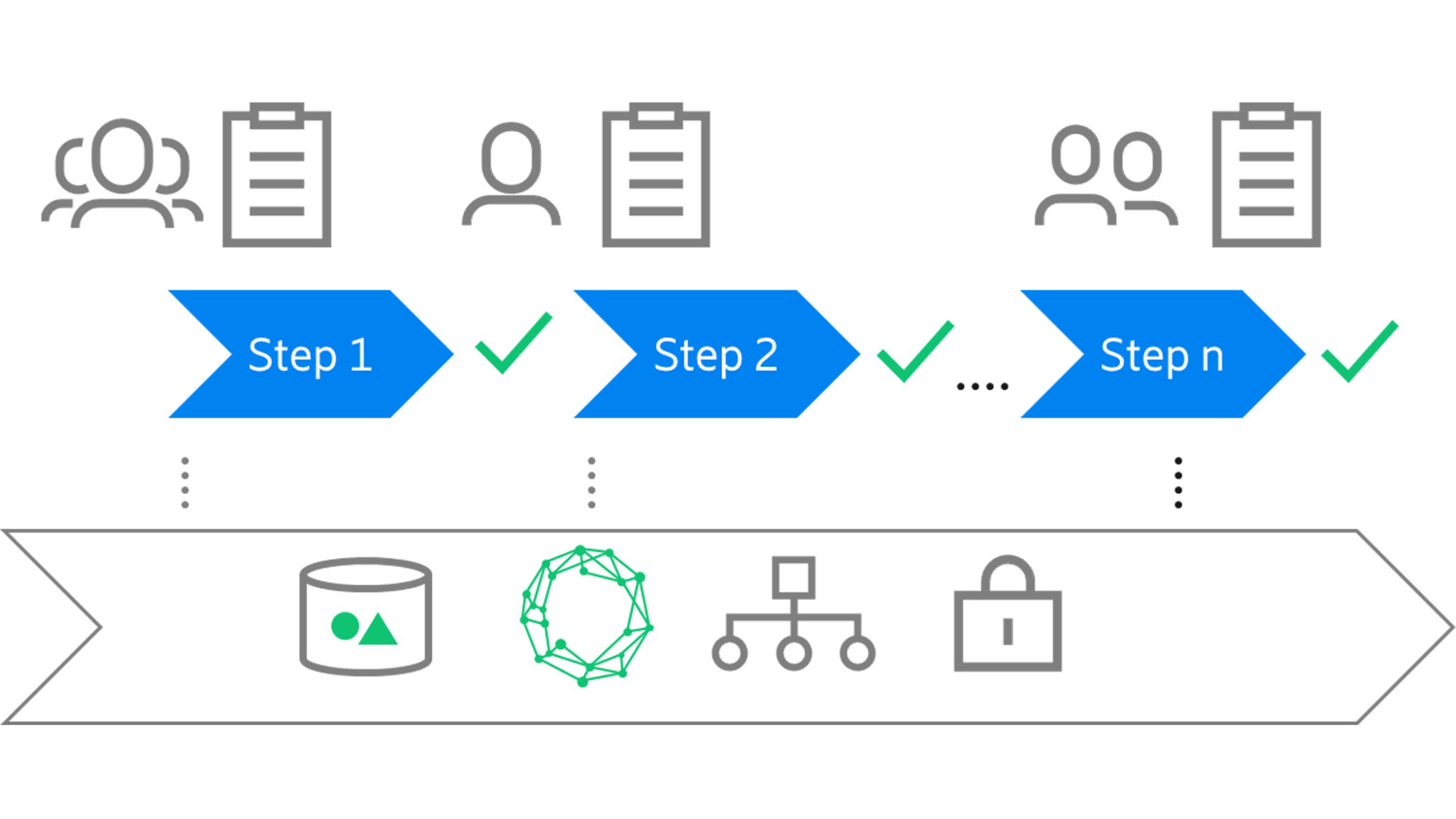

Moreover, the policy and related procedure of the process can be coded in smart contracts, ensuring high compliance and the standardization of the process. It can also prevent any unauthorized member to access or execute a process that is not in accordance with the predefined procedures and their rules. Validation happens step-by-step, preventing any potential flaw in the process.

Figure 2: Step-by-step validation prevents any potential flaw in the process.

In other words, as long as the policy of any business process and its procedures are well coded in smart contracts, blockchain can secure the perfect execution of any business process, both cross-organizations (within the same company) and cross-company.

Last but not least, every record in the ledger embeds a chronological timestamp – securing full traceability – as well as the digital signature of the parties agreeing on the record (also known as ‘non repudiation’).

The above can generally be applied to any business process, creating potentially zero-fault business executions, and digitalized end-to-end through blockchain automation and integration with legacy systems.

Figure 3. Mapping of business process flaws with blockchain capabilities.

Our first successfully implemented use case was quite a familiar process in corporate finance: Intercompany Invoice. Today, it’s in full production globally as the sole solution, covering more than 180 countries where Ericsson operates, supporting the business process. Many of the current blockchain implementations in the market have been claimed to be “shadowed”, i.e. running in parallel with traditional ways of working.

The Intercompany Invoice process was affected by many of the flaws already mentioned. But by leveraging blockchain capabilities, we were able to prevent the characterized issues upfront, rather than fixing them afterwards. Today, it’s fully automated and involves minimal human intervention. This means tedious manual jobs are avoided, and enforces a common way of working between all the parties involved, ensuring high efficiency and Return of Investment.

By following this method, Ericsson can keep implementing highly impactful business processes through blockchain technology, and produce unprecedented efficiency and zero-touch automation.

It’s automation at the next level.

References

Morris, David Z. (21 January 2014). “Bitcoin is not just digital currency. It’s Napster for finance”. Fortune. Retrieved 7 November 2018.

Schulpen, Ruben R.W.H.G. (1 August 2018). “Smart contracts in the Netherlands – University of Tilburg”. uvt.nl. Twente University. Retrieved 26 October 2019.

Learn more

Read our blog post, 5G and blockchain: The building blocks of the shared economy.

Read the Ericsson Technology Review article, Facilitating online trust with blockchains.

Find out whether we can put our trust in a decentralized marketplace